Boku Inc. (LON: BOKU), the world’s leading independent direct carrier billing company, today announced its final audited results for the year ended 31 December 2018.

Financial Highlights

· Revenue up 45% to $35.3m (2017: $24.4m)

· Adjusted EBITDA $6.3m vs. 2017 Adjusted EBITDA** loss ($2.3m)

· Reported Net loss of $4.3m down 85% (2017: $28.1m)

· $32.3m Gross cash at year end (31 December 2017: $20.2m)

· Monthly average cash balances of $24.4m (2017: $19.2m)

Operational Highlights

· Total Payment Volume (TPV) doubled to over $3.6bn (2017: $1.7 billion)

· 13.5 million Monthly Active Users (MAU) in December 2018 (December 2017: 8.0 million)

· 70 new Boku Account connections for major customers such as Apple, Microsoft and Spotify (2017: 45)

· Acquisition of mobile identity business, Danal Inc.on 1 January 2019

**Adjusted EBITDA: Earnings before interest, tax, depreciation and amortisation, adjusted for stock option expenses, forex gains/losses and exceptional items

Jon Prideaux, Chief Executive of Boku Inc, commented:

“2018 has been a transformational year for Boku; two major milestones include reporting our maiden positive Adjusted EBITDA for the whole year and the acquisition of mobile identity business, Danal Inc. We’ve delivered growth on all of our KPIs illustrated at both the top and bottom lines.

“We believe that 2019 will be another year of exceptional growth as we continue to build upon our strong Payments business, growing Identity business, and our state of the art platform to deliver further products and services to our customers.”

Capital Markets Day

Boku will hold a Capital Markets Day for institutional investors and analysts on Wednesday 22 May 2019. The event will be held in London, with the venue and timing to be confirmed. Further details will be provided in due course.

Chairman’s Statement

2018 has been a year of growth and expansion for Boku. Volumes processed through the platform have more than doubled to $3.6 billion, further strengthening our lead as the world’s largest independent carrier billing company. New customers like Netflix and Rakuten have started to use our platform and existing customers like Sony, Spotify and Apple have expanded their use. Revenues have increased by 45% and for the first time adjusted EBITDA was positive for the whole year.

This increasing scale is a source of considerable competitive advantage to the Company. As a platform business, where incremental transactions can be processed for minimal marginal expense, higher volumes drive lower unit costs. This makes Boku a difficult company with which to compete.

The real value that we provide to our customers is to help them acquire new paying users and so it is a source of real pride that the number of Monthly Active Users making payments on the Boku Platform has increased to more than 13.5 million in December 2018, an increase of 66% over December 2017.

Last year I indicated that the Company was looking to invest in new capabilities that would allow new value to be unlocked from the platform. The acquisition of Danal Inc., completed on 1 January 2019, which makes the Company a leading player in the Mobile Identity market is just such an opportunity. Boku, by virtue of this acquisition, is now able to diversify its addressable market beyond digitally downloaded content to also include electronic remittances, mobile payments, on-demand services, online banking and government services. This application of our platform will drive future growth and lessen the risk of revenue concentration.

I want to thank my fellow Non-Executive Directors for their service throughout the year. Both Richard Hargreaves who chairs the Remuneration Committee and Keith Butcher who performs a similar function for the Audit Committee have been generous with their time and expertise to help the Company make the most of its public company position.

2019 will be another pivotal year. We have embarked on a course designed to help us diversify from being a single product company to become one with multiple products driven from our state-of-the-art platform. The management have developed the organisation to the point of profitability, and I have every confidence in their ability to help it achieve its potential.

I look forward to seeing yet further significant growth over the course of the next year.

Mark Britto

Non-Executive Chairman

25 March 2019

Chief Executive Officer’s Report

2018 has been a stellar year for Boku. The volume of payments processed by the Boku Platform more than doubled. Revenues increased by 45%, costs grew only modestly, and the result was the Company’s maiden positive Adjusted EBITDA for the whole year.

Looking to the future, our Payments business is on a steady growth trajectory. Operating in an expanding market, with most of the largest digital companies as customers, our growth is underpinned by their success. But, more than this, our business will benefit from an increased number of connections; in 2018 the number of our most advanced, Boku Account, connections increased to 177, enabling Boku payment for many millions of new subscribers.

These connections have now only started to yield their potential volume and revenue: once launched, subscribers only gradually discover our service as they attempt to make purchases. As a result, a two-year maturity cycle applies, meaning that the 109% TPV growth that we reported for 2018 is a consequence of the deployments that we made in the preceding two years, and the deployments undertaken this year still have two more years of growth to deliver.

Taken together, this provides a platform for steady growth with a predictable profile.

The Boku Payments business is generating more recurring revenue from returning users. Our users now fall into three categories, one-off; regular subscriptions and pseudo-subscriptions, like the app stores, where consumers repeatedly (though not necessarily regularly) make transactions using their phone number as their stored payment credential. This recurring revenue helps boost our volume. Every month around 1.5 million users make their first Boku transaction; with increasing numbers of them transacting repeatedly, growth continues to compound.

With gross profit margins at 93% (2017: 91%) and plentiful growth on predictable trends it would be easy to be complacent. It’s tempting to play things safe. Tempting, but wrong.

A company can strive to breakthrough to profitability for years. On reaching profitability, a company is typically congratulated however, the point of profitability is a dangerous time. The company is faced with a choice: does it settle for what it has, or carry on investing for growth? Does one reap or sow?

All things must pass. The growth achieved from pursuing one application of Boku’s platform will inevitably, eventually peak over time. Not this year or next, but inevitably the S curve will start to asymptote, level off, slow down.

So, Boku has chosen a path of growth: we have built a platform which brings together the world’s largest connected community and for now, most of our revenue comes from using it to help people sign up smoothly to digital services. We’re powering app stores. We’re helping digital music services to grow their premium users, streaming video companies come to us to help them grow their user bases too. But collectively these sectors account for only 5% of global e-commerce.

Our technology can help more than 5% of commerce – our imperative is to build out our platform to be able to service new merchant segments including Finance, Payments, Money Transfer, Governments and On-demand services; to provide these organisations with a way for their customers to transact on mobile with security and ease of use; to address a bigger market and to embrace the bigger trend, not just the movement to digital entertainment, but to embrace the wider movement to mobile transactions.

Our acquisition of Danal Inc. should be seen in this context. It is the springboard that will enable us to repeat our trick of becoming the globally dominant player in our segment driven by our access to carrier assets. With a great platform, strong channel partners and identity connections already live with carriers in North America and Europe, we have acquired a business at a point of inflection that has signed up important customers and is ready to deploy its services more broadly, within a market that is experiencing substantial growth.

Faced with the choice of reaping or sowing, we have chosen the path of investment; to expand our business, take some of the cash that is being generated from the Payments Business and build a second business line, Identity, on the Boku Platform; to utilise the same skills, carrier connections and sales approach to build a second strand of Carrier Commerce.

Outlook

We look forward to 2019 with enormous optimism. In the next 12 months, Boku will operate with multiple product lines across a broader set of customers, adding value to a greater proportion of mobile commerce. For 2019, we anticipate that continued growth in our Payments Business and investment in Identity will deliver Revenues of at least the current analyst consensus of $52 million, with 15% to 20% of this coming from Identity. Trading in Identity has so far been encouraging with a significant contract signed in February. Gross Margins in Payments are projected to remain strong at 93%, those in the Identity business will strengthen to c.40%.

We expect Adjusted EBITDA to grow by 45-50%, driven by underlying performance and the implementation of IFRS 16 ($1.9 million).

Our forecast is for a record year: record revenues, record EBITDA, investment in new products and continued cash generation. And this is just the start, our flexible platform allows us to roll out new products into other sectors, to make more mobile transactions simple. Truly, the journey has just begun.

Jon Prideaux

Chief Executive Officer

Date 25 March 2019

Chief Financial Officer’s Report

2018 was the year that Boku became a multi-product business, with significant investment in Mobile Identity services, culminating in the acquisition of Danal Inc.

What is pleasing about our 2018 results is the degree of predictability in our Payments division. We help our merchants to acquire new paying users, these users in turn consume digital products and this drives our TPV number. TPV is the raw material from which we generate revenue. The other key ingredient to our revenue is the take rate – for the year to December 2018 our weighted average take rate fell at a far slower rate from 1.4% in 2017 (compared to 3.1% to 1.4% between 2016 and 2017). This decline was fully anticipated and reflects a mix of business and volume related discounts for certain clients.

Net Loss

The Company reported a Net Loss for the year of $4.3 million, an improvement of 85% compared to the $28.7 million the net loss posted in 2017 (2017 included costs of Admission to AIM and the conversion of convertible notes. Net of these costs, 2017 Net Loss would have been $7.4 million). Net Profitability in 2018 was influenced by a change in accounting for Employee Long Term Incentives (up $3.1 million on 2017 driven by a higher company share price and a change in accounting policy for tax on share-based payments), a write down of a deferred tax asset ($1.1 million), the costs of acquiring Danal Inc ($0.4 million) and some internal restructuring costs ($0.6 million).

When adjusted for the above items, the Net Profit would have been a $1.3 million for 2018 (please refer to note 4 to the financial statements for further details).

Revenue and Gross Margin

Revenue for the year of $35.3 million was up by 45% on 2017. This performance was driven by overall TPV growth and average weighted take rates that held up at 1%.

Strong growth from our App Store clients was balanced with an equally buoyant performance by our Settlement business portfolio. The Company benefitted from exposure across all channels to market phenomena such as FIFA, Fortnite and general growth in the market for Digital products and services.

Having a mixed portfolio of customers in Music Subscriptions, Movies, Games, Social Media, in addition to supporting both direct and indirect channels, helps to maintain a reasonable margin mix.

Mix of business combined with continued buying prowess helped gross profit margin continue to increase to 93% up from 91% in the previous year. Gross Profit therefore climbed 48% on revenue that was up 45%.

Operating Expenditure

Adjusted Operating Expenditure (Operating Expenditure adjusted for depreciation, amortisation, foreign exchange, stock option expense, exceptional items, loss on disposal of property and restructuring costs) increased by 8% to $26.4 million in 2018 (2017: $24.5 million). The 2018 increase was mostly driven by the Group’s £1.5 million of seed investment in Boku Labs and Boku Mobile Identity. Please refer to note 5 for details.

Underlying expenditure in the core Payments Business grew by just $0.4 million (2% higher than 2017). The majority of this increase resulted from a modest investment in our core payments infrastructure, more specifically a data centre upgrade project which increased the latent processing capacity of the Boku platform to now be capable of processing at up to 600 transactions per second (TPS) (current highest peak is 216 TPS).

From 1st January 2019 onwards, costs relating to Operating Leases will be required to be capitalised and amortised below EBITDA under IFRS16. This will have the effect of increasing the Company’s EBITDA going forward (please refer to Note 1 of the Financial Statements for further details).

Operating Result

Reported Operating Losses for 2018 of $2.4 million were down from $9.0 million in 2017. This can be broken down as follows:

· Foreign Exchange movements caused a small ($0.3 million) charge to the P&L compared to a $0.4 million gain in 2017.

· Stock Option Expenses – The Company recognised costs of $4.6 million in 2018 compared with $1.5 million in 2017. Of the $4.6 million booked in 2018, $1.0 million was paid out in cash (via employers NI), the remainder was non-cash and expensed per below:

o During 2018 the Company introduced a new Employee Equity Scheme to retain and reward employees. Within the scheme, share awards for senior management are deferred by 3 years and are “paid out” in line with company performance against Adjusted EBITDA/share targets.

o Due to the high share price on the date of issuing the RSU grants (September 2018: $2.24; 2017: $0.37 pence per share) to the employees and executives the share-based compensation expense is far higher than in previous years (2018: $3.4 million; 2017: $909,000).

o The 2018 expense is highly influenced by the change in accounting policy for accrued employer payroll taxes on issued share options (see note 2).

· Exceptional Items improved from $2.6 million of cost to $1.1 million of cost between 2017 and 2018 In 2018. Exceptional Items incorporated the cost of acquiring Danal Inc ($0.4 million, which mostly includes the legal costs incurred prior to the acquisition of Danal on 1January 2019) and the cost of closing a surplus legal entity in Italy ($0.6 million). In 2017 exceptional items included costs relating to the Admission on AIM ($2.1 million).

Adjusted EBITDA improved from a loss of $2.3 million in 2017 to a profit off $6.3 million in 2018.

Financing Expenses

Net financing expense reduced significantly from $19.6 million in 2017 to $0.6 million in 2018. The 2018 cost includes the one-time costs of $0.1 million to early exit a German factoring facility in Q1 2018.

In addition, the working capital debt facility was paid down to minimum interest levels ($2.2 million) in Q1 2018.

Run rate interest expenses are just $15,000 per month as at December 2018.

2017 Finance expenses include the finance costs related to Convertible Notes which were converted into common stock at the Admission to AIM ($17.1 million).

Balance Sheet and Cashflow

The Company strengthened its cashflow in 2018 which can be demonstrated by its closing cash balances increasing to $32.3 million at the end of 2018 from $20.2 million at 31 December 2017.

Monthly average cash balances, which smooth the impact of intra-month flows of both carrier and merchant payments, climbed to $24.4 million in December 2018 from $19.2 million in December 2017, proving that Adjusted EBITDA performance is starting to convert into cash. Cash generated from Operations during the year was $13.5 million.

From a working capital perspective, Current Assets exceeded Current Liabilities at 31 December 2018 by $4.4 million compared with $1.3 million at the 2017 year end.

The working capital loan facility was reduced from $2.4 million to $2.2 million during 2018. Net Cash was $30.1 million at the end of 2018 (31 December 2017: $18.7 million).

Intangible Assets were reduced to $22.5 million over the period, down from $25.8 million at December 2017 reflecting annual amortisation. Remaining intangible assets include $17.9 million of Goodwill emanating from historical acquisitions.

Looking Ahead and the Acquisition of Danal Inc

The Company successfully concluded the acquisition of Danal Inc, effective 1 January 2019. The transaction will help the company to springboard plans to widen its addressable target market exponentially, beyond digitally downloaded content and into broader m-commerce.

Danal was acquired for 26.7 million Boku shares (equal to 10.7% of the enlarged share capital) with posted 2018 revenues of $5.3 million and expected strong revenue growth in2019 delivered through a material sales pipeline. A further payment in Boku shares and warrants will be made, on a ratcheted basis, should the acquired business deliver above $10.0 million in revenues during 2019. Any such payment or further issue of shares would be made in the financial year ending 31 December 2020. As of the approval of the Annual Report, the Group is finalizing its evaluation of the purchase price accounting relating to the acquisition and an update will be provided at the Group’s forthcoming interim announcement.

Revenue upside will be delivered through accelerated global roll out to carriers with whom Boku already has a relationship and cross sell opportunities into Boku’s existing merchant base.

The Company expects the acquisition to be Group EBITDA accretive from 2020 onwards.

Aside from investment in Mobile Identity, the Company expects to see continued growth in its core Payments business and will be making investments in new product developments in Payments to sustain this growth. This will be funded through a modest increase in Operating Expenses and by reallocating existing resources as they roll off current projects.

Stuart Neal

Chief Financial Officer

Date: 25 March 2019

Market Review

Mobile Phones – the start of the usage revolution

Andreessen Horowitz, a leading venture capital firm and shareholder in the company, made a presentation in 2016 called “Mobile is eating the world” and another in 2018 called the “End of the beginning”. The thesis of the presentations was that whilst we are well on the way to distributing smartphones to all adults on the planet, the usage of those devices, which signals the start of a new computing paradigm, has only just begun.

Use of the mobile device in commerce is growing rapidly – for example, 40% of Amazon’s sales in the US during the 2018 Holiday season were initiated on a phone. In Asian countries, like India and China, where internet adoption happened primarily on mobile, not PC, the percentages are much higher. Despite this, Andreessen Horowitz argues, we are still a long way short of achieving usage to match the distribution.

This shift from distribution to usage is evident in Apple’s change of emphasis from a business that grows primarily by selling new iPhones to one that grows by selling more services to the existing base of iPhone customers.

The distribution task is basically over. But mass usage is just beginning.

This unprecedented, global deployment of computing power has created a new, mobile-centric economy. As usage increases, an ever-wider selection of goods and services will be bought and sold on the smart phone. Online retail, digital entertainment, on-demand services, and even interactions with Governments are undertaken on mobile, and every one of those interactions – which embrace the whole lifecycle including enrolment, login, purchase, and regular usage — needs to be easy for the user and secure for the supplier.

Mobile Phone vs PC – a different paradigm

Transacting on mobile is not the same as transacting on a PC, just with a smaller screen. Many problems that have been solved for the PC need to be solved again for mobile. To illustrate this in a small way: most e-Commerce services use your email address as your identifier. But many people who have come to the internet in a mobile-first environment don’t have an email address, or prefer not to use it. They use WhatsApp or WeChat or Facebook Messenger to communicate. The index of their digital identity is not their email address, it’s their mobile phone number.

The smartphone changes the user interface. It’s hard enough to type in 16 digits of your card number on a keyboard (and the 4-digit expiry date and the 3-digit CVV and quite possibly your name and address too), but, on the glass of a smartphone, it’s positively painful.

On the other hand, mobile phones offer many unique advantages – they are always with the user, they can be geo-located, they have multiple sensors including built-in cameras, Bluetooth antennae, biometric readers, and a network connection that allows the user to download, install, and run countless apps from anywhere in a matter of seconds. These advantages offer the potential for a completely new user experience.

Disruption across Multiple Industries

This new mobile computing paradigm is disrupting industry after industry at every stage of the customer lifecycle. How you get your bank account; the way that transportation services are delivered; the fact that you’re prepared to register to consume music or watch films; the way you play games and how you pay for them; how you book hotel rooms how you book a restaurant or order a takeaway. All these experiences are different today because we have in our pockets a location aware, user-friendly computer that is connected to the internet at all times.

The move to mobile has, in particular, disrupted entertainment: the digitisation of games, music and video has proceeded apace. The old media of CDs and DVDs have become all but obsolete. There is a landgrab underway, with new and established players trying to sign up as many new users as possible. Removing friction from the sign-up process and accessing as many users as possible became necessary parts of the armoury for any serious digital content provider. Providing solutions for merchants in this area has been Boku’s initial focus.

But mobile disruption doesn’t just apply to digital, it applies to all types of transaction. As more business transactions across more market sectors migrate to mobile, the same challenges that faced digital content merchants now apply to a much wider range of other businesses – the need to attract and retain high quality users is universal.

Risk and fraud solutions developed for the PC world don’t always address the problems of mobile: One-time PINs can be intercepted with social engineering or malware, apps can be hacked, logins can be phished, and phones, especially those running Android, can be rooted and compromised. The result: increasingly large-scale abuse and fraud on mobile. Legacy anti-fraud solutions typically add friction to transactions. What is needed is a way to deliver security with low friction on mobile. This is the next area where Boku is providing solutions.

The Value of Mobile Operator Networks

What these two examples show is that as more businesses transition to mobile, the need will grow for simple, secure ways to acquire new customers, verify their identity, provision services onto the handset and detect threats in real time. Because these transactions all happen on mobile devices, Mobile Network Operators hold the key.

Central to the Mobile Network Operator’s ability to secure and authorise voice and data connections is the SIM card. The SIM card provides every mobile phone in the world with a secure element owned by the Mobile Operator. The Mobile Operator can verify that secure element, silently, in real-time; they can detect your mobile number without having to ask for it. In most instances, they also know who you are, know information about your mobile device, know information about your payment or top-up history, and can facilitate financial transactions by leveraging the existing billing relationship they’ve set up with each mobile subscriber. These assets provide a powerful and essential collection of tools for enabling this new era of mobile usage.

Mobile Network Operators may hold the keys that can unlock much of this latent potential, but they need Boku’s help to commercialise these unique assets because, in practice, these capabilities are inaccessible and fragmented behind the hundreds of different back office systems. It’s easy for consumers to make phone calls and send text messages, but it is nearly impossible for businesses trying to access any other Mobile Network capability to independently connect to the multitude of different Mobile Operator systems.

The Boku Platform

Boku has developed a platform to solve the problem of accessing and monetising these hard-to-reach mobile assets. By connecting to the user-facing systems of Mobile Operators around the world, we build products, delivered via simple-to-use APIs that enable enterprise customers to transform the mobile experience for their users and power the growth of their business.

With Boku as the trusted intermediary, we can make the power of Mobile Networks available to the world’s app developers, businesses and governments.

Other solutions try to deliver low friction approaches, but they require registration; with Boku you registered when you got the phone.

The Boku Platform can use Mobile Network Operator and other systems silently to:

· authenticate the handset;

· gather information about the device;

· check the user’s eligibility for different services;

· charge and credit the user;

· collect and disburse aggregated funds in multiple currencies from multiple countries;

· provide new services onto mobile subscriptions;

· provide coarse or fine location data for devices;

· expose certain characteristics of the customer profile including pre-paid/post-paid and length of tenure;

· send and receive messages

These raw ingredients can be combined in different ways to produce a myriad of products that solve problems for merchants.

While it is carrier information that provides the Boku Platform with much of its distinctive character, the platform is also effective in aggregating and harmonizing mobile capabilities that come from other non-carrier sources. In mobile payment, these additional payment methods can enhance the offer by providing alternative sources of funds when the carrier bill is not appropriate or economic. Combining carrier identity data with other sources can deliver an even higher level of security or insight.

The Boku Platform: Mobile Transactions Made Simple

Our platform is a powerful asset. Initially used to help companies distributing digital content acquire new customers, its capabilities can just as easily be applied to other aspects of the customer journey and to other industries. Whether it’s retaining customers through prompted messaging, preventing the abuse of marketing promotions, validating the users that access a service or delivering the service to the right device, all aspects of the customer journey can be enhanced by the Boku Platform.

At scale. Globally. Across multiple industries.

Having applied our technology to solving customer acquisition for digital content, we now have the tools and capabilities that can be applied to other parts of the value chain and across multiple other sectors. We have started already by delivering mobile fraud and identity solutions for Banking, Money Transfer and On-Demand Services, and, once we have established strong presence in these markets, we will repeat the process again in new sectors, applying the power of our Platform that connects billions of consumers through their most personal ubiquitous device to simplify more aspects of mobile commerce.

The Benefits of Scale

To attract the biggest merchants, Boku built a global organisation and a high function platform which meets the needs of many merchants. These merchants bring us the highest volumes of transactions, which in turn, yield the lowest unit cost in the industry. In the last two years, as the volume of successful transactions processed through the Boku Platform has more than tripled, unit costs have reduced by nearly three quarters. Further growth is possible at modest cost: in the course of 2018, capacity was increased by 55% for an expenditure of less than $330,000.

Bigger is also better: Boku’s scale brings more data to optimise performance. For example, the value of transactions processed through a single merchant-carrier connection increased by 37% after it was moved to the Boku Platform, through the use of Boku’s optimisation tools. On average, a Merchant that uses our Platform can expect to see its volume increase by more than 20%. These economies and advantages apply across multiple products – success in Payments means better Identity products. Wider coverage for one application helps another.

Carrier Network

The carrier network that Boku has built over 10 years with an investment of more than $100m is hard to replicate. The unparalleled level and quality of carrier connections that we enjoy is a consequence of the merchant connections that we have been able to acquire. Because each carrier connection is unique it would be very hard, if not impossible, for anyone else, even had they the resources, to be able to copy the breadth and depth of our carrier network.

Global Merchant Base

Boku has developed an unrivalled network of Global brands as customers. Companies like Apple, Facebook, Microsoft, Netflix, PayPal, Rakuten, Sony, Spotify, Square, Uber and Western Union all trust Boku to be their Partner. With 13 offices in 10 countries Boku has developed the global coverage and the way of working that makes us the natural choice for any organisation looking to access the power of mobile operator networks globally.

Boku Payments For Digital Goods

The market for digital content paid for by carrier billing is estimated by Ovum at $26 billion in 2018, growing at 11% CAGR (Compound Average Growth Rate).

Target Merchants

Many of the world’s largest digital retailers including app stores, like Apple and Google, console makers like Microsoft and Sony, and streaming companies like Spotify and Netflix, utilise Boku, as do the leading MMO (massive multiplayer online) game publishers such as Activision Blizzard and Tencent Riot, social gaming platforms such as Facebook Games, and gaming PSPs (payment service provider) such as Xsolla. We are also seeking to extend our reach in Asia, targeting companies from China, Korea and Japan to help them acquire new users, especially as they seek to expand abroad.

Merchant Benefits

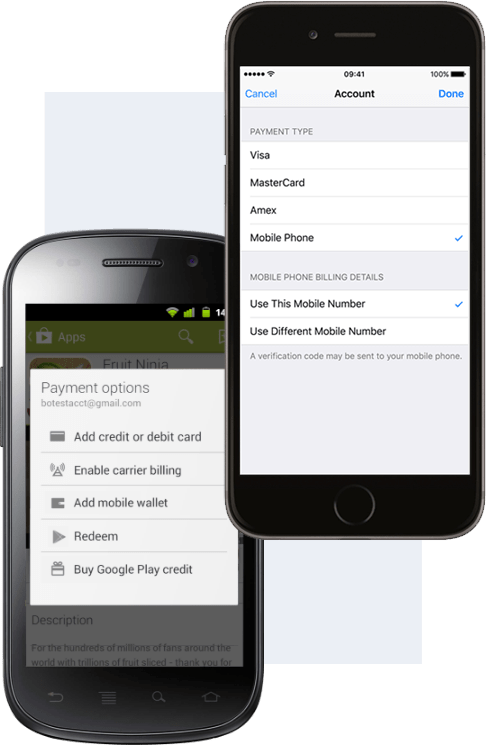

Boku Payments help digital merchants recruit new users. Oftentimes, users only need a single tap to set their phone number as their payment credential, improving conversion rates. Whilst charging to your phone bill is an expensive means of payment for merchants compared to bank-provided alternatives, it is a cost-effective means of acquiring new users.

Business Model and Revenues

Boku Payments have processed over $3.6 billion of transactions in 2018 and accounted for all the revenue generated by the Boku Group in 2018 at $35.3 million, an increase of 45% compared to the previous year.

Fees are charged as a percentage of the overall transaction value with some differences between customers depending on whether Boku handles the funds (the settlement model) or acts solely as a technical processor (transaction model). Some merchants also receive volume discounts as part of their pricing scheme. Take rates (re divided by total payment volume) averaged 1% for the year. The rate of reduction has stabilised, following reductions in prior years driven by a change in the mix between the settlement and transaction business models.

Growth Drivers

In 2018, Boku’s volume grew by 109% to more than $3.6bn of value processed, a relatively modest penetration of a large and growing market. The disruption of digital has only just begun. App store growth is forecast at 18% CAGR, which provides a strong tailwind for Boku who already processes 40% of the carrier billed volume coming from app stores. Further growth comes from Boku increasing the number of Boku Account connections*, thereby making the service more widely available. These connections increased to 177 by the end of the year an increase of 65% on 2017’s closing figure of 107. Each new connection starts a process of discovery of the Boku payment option amongst that carrier’s customers, a process that typically continues for two years. Further growth can also be anticipated from new customers and new funding sources being added to the Boku Platform. In short: super-normal growth is baked in.

Competitive Advantage

Boku’s advantage lies in its scale. Having more merchants helps us get the best connections from carriers with the best commercial conditions. In turn, this helps us to recruit more merchants which drives up our transaction volumes and provides us a richer data set for performance optimisation. Similarly, the fact that we have a wider breadth of merchants and a larger scale of volume than any other provider means that we can simultaneously have the broadest range of functionality and the lowest unit costs.

*Connections relate to the link between the merchant and the carrier

Boku Identity

The acquisition of Danal Inc., now renamed Boku Identity Inc., was completed on 1 January 2019.

McKinsey estimates the size of the Identity-as-a-Service at $10 billion in 2017, growing to $16 billion –$20 billion in 2022 (9-15% CAGR).

Geographically, all parts of the world are exhibiting growth, but this is particularly pronounced in Asia, where identity data is hard to source; mobile is the predominant channel for internet access giving Mobile Operator data a distinct advantage.

Target Merchants

Any organisation transacting on a mobile device or wanting to analyse the mobile behaviour of their users is a potential customer for Boku Identity. Boku is particularly focused on organisations in the Payments, Money Transfer, Banking, On-Demand Services and Government sectors.

Customers of Danal Inc. include PayPal, Square, Western Union, MoneyGram, JP Morgan Chase, BNP Paribas, Uber and the US Government’s Internal Revenue Service.

Merchant Benefits

Historically there has been a trade-off between ease of use and security. Increase security and you introduce friction which can drive away potential customers; provide a simple user experience and leave yourself vulnerable to fraud. Boku Identity products allow security with no friction, because the Mobile Operator knows your phone number without having to ask. Using the secure SIM card as your identity, combined with other back office data held by the Mobile Operator, can reduce fraud and ensure compliance without needing to inconvenience the end user.

Use cases:

– Secure, frictionless 2 Factor Authentication: Silently validate a mobile device without the need for an SMS, using automatic mobile number verification

– Know Your Customer: Streamline the KYC process by validating the name and address entered by a user against Mobile Operator data

– Promotion abuse: Reduce offer fraud by linking marketing promotions to secure SIM-based user identities instead of email or unverified mobile numbers

– Account Takeover Prevention: Pro-actively monitor and detect SIM card changes to prevent SIM swap fraud

– Credit card and bank fraud: Reduce fraud by providing real-time Mobile Operator data as risk inputs for enterprise risk and fraud systems

– CRM data compliance: Ensure compliance with consumer regulations by validating phone number ownership and monitoring for phone deactivations and number transfers

Business Model and Revenues

Merchants are charged either on a per user basis – for monitoring – or on a per transaction basis, typically with monthly minimum amounts. In December 2018, 12.2 million numbers were being monitored. 175 million billable transactions processed in 2018, a 95% increase on the number processed in 2017. At present charges are predominantly for data elements, over time it is intended to introduce premium pricing for higher value, packaged products.

Danal revenues amounted to $5.3 million in 2018 (pro-forma, these unaudited revenues were reported by Danal Inc. prior to its acquisition by Boku on 1 January), a modest increase from $5.1 million in 2017, generated from the provision of mobile identity and compliance services to customers predominantly in the United States.

Growth Drivers

As mobile transactions increase, demand for mobile identity solutions is increasing in lockstep. There is plentiful demand. Growth is constrained by supply of carrier data and sales capacity. Both of these are addressed by integrating Boku Identity into the Boku Group. Supply can be increased by Boku’s capacity to source and build new connections at global scale – 20 new connections are planned for 2019. Sales capacity is being tripled, with more account management and business development staff being hired.

Competitive advantage

Traditional identity providers have tended to connect to large static databases, which are optimised for PC-based e-Commerce. Boku Identity’s connections provide access to the unique Mobile Operator data set which provides real-time information about a customer’s status, all without interrupting the user experience.

Boku Identity is able to leverage the existing network of Mobile Operator relationships and connection capabilities developed by Boku Payments in order to expand into to new markets faster than any competitor.