Boku Inc (LON:BOKU) Chief Executive Officer Jon Prideaux caught up with DirectorsTalk for an exclusive interview to discuss the company’s background, how it derives its revenues, why they chose to float on the AIM market, how they differ from competitors and his view on the next few months for the company.

Q1: Boku listed on AIM this week, could you explain for us the background to the company?

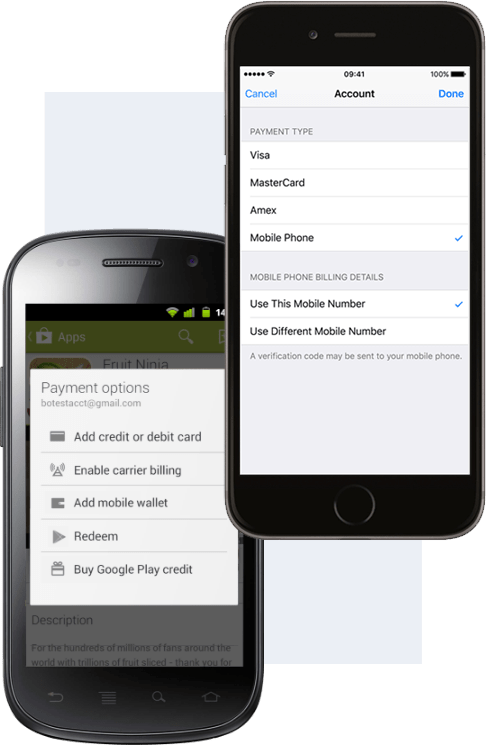

A1: So, the business concept is really pretty simple, we allow people to buy things and charge it to their mobile phone account, whether that’s pre-paid or post-paid. The reason that’s a good idea is it’s just a heck of a lot easier if you’re on you mobile to use your mobile number as the payment, it’s just a lot more convenient.

You just think about fiddling around, typing in 16 digits of a card number on your smart phone and you can understand that you’re going to have a much higher conversion if you can just tap once on the screen in order to be able to subscribe to Spotify, for example, and that’s the type of technology that we can provide.

So, our customers, who are the likes of Spotify, Apple Inc (NASDAQ:AAPL), Sony Corp [ADR] (NYSE:SNE), Microsoft Corporation (NASDAQ:MSFT) and Facebook Inc (NASDAQ:FB), they come to us because we help them to acquire new paying users that they wouldn’t get any other way.

Q2: So, Boku collects payments using a mobile phone, how does it derive its revenue?

A2: As I say, we have a lot of arrangements with mobile network operators around the world, so we’re connected to about 170 mobile network operators in around 50 countries. We make our money in two basic ways, every time, we take a percentage of the value that flows through the system and the amount that we take really depends on how big a job that we do.

So, in certain instances, a really big company like Apple or Google (Alphabet Inc -NASDAQ:GOOGL) , they already have all the commercial interaction with mobile phone companies, so they come to us to do a transaction processing job and there’s one level of fee for that.

Other companies like Spotify, Sony, Facebook, they rely on us to negotiate the contracts with the carriers to collect the funds, to handle to currency conversion and do the transaction processing and therefore we can obviously make a somewhat higher margin on that because we’re doing more.

The basic way in which we make money is very simple, we just take a piece of the value that flows through our system.

Q3: Why is it that Boku chose to float on the AIM market in London?

A3: It’s a good question, I mean at some level we’re fairly ‘classical, Silicon Valley, venture backed company’ but we were persuaded that for a company of our size that being a bigger fish on AIM would extract better value and attention from the market than would be the case for being a small organisation for example of Nasdaq. For what it’s worth, I think investors in London do understand this market somewhat better and given the reaction we’ve had to our IPO, which was frankly very much over-subscribed, and I think that turned out to be a very good idea.

Q4: Bango, a similar company, has been listed for some time, how do you compare?

A4: First thing to say is in-payment scale is important and the reason why scale is important is that it allows you to be at one at the time, the low-cost player and the high-cost player so both are as much bigger than Bango.

I can’t remember Bango’s latest reported figures but if you take our annualised payment volume based on our September number, we’re processing at a run-rate of about $2.3 billion and on revenues that were in 2016, we were just around $17 million worth of revenue. Those are figures that are materially larger than Bango and what that means is that our cost per transaction when we amortize that across our cost base, as far as we can tell, if their transaction fee was the same as ours, we’d be about half those at Bango.

So, one at the same, we’re the low-cost player and then on the other side of the coin, we can carry much much bigger cost because it allows to us to provide more function. We can do this transaction model processing as well as settlement, we can have people in the field to help companies that don’t have the bandwidth to go out and do deals with, for example, companies in Japan or in India or in the Middle East, and we can put people on the ground to help with that process, we can also invest more in innovation.

So, we’ve become quite a tough company to compete with, you try and compete with us on price you’ll find we’ve got a lower unit cost, you try and compete with us on function you’ll find we’ve probably already got the function that you’re talking about and if we haven’t, we’ve got 87 or so technical staff that will be able to build it very quickly.

The key weapon I think that we have that means that Boku is the leading company of our type is our scale and that scale will, over time, mean that somehow the big get bigger.

Q5: Now, you’ve obviously gathered a fair bit of attention, how do you view the next few months for Boku Inc?

A5: Well, I think that we’ve had a lot of interest, as you say, and it’s now incumbent on us to be able to execute our plan and continue to grow. We passed an important milestone of being EBITDA-positive so we’re looking clearly at not only improving results in terms of the value that we process and in some respects that’s a vanity measure. What we would want to look at is continuing to improve our revenues, keep a close eye on our cost within the constraints of wanting to be able to still be a full-service player and then just deliver through better bottom line results for the investors to have chosen to invest in Boku.