Anglo American plc (LON:AAL) has announced its production report for the third quarter ended 30 September 2025

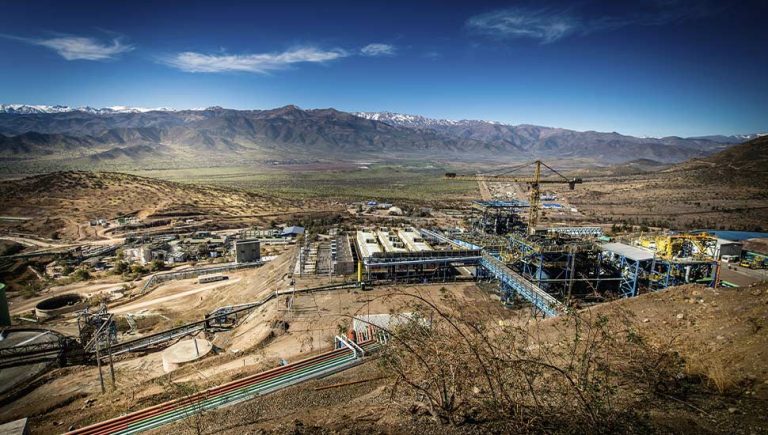

Duncan Wanblad, CEO of Anglo American, said: “We’ve delivered another solid quarter in Copper and Iron Ore, tracking to our plans and we are well positioned to meet 2025 guidance, with the full year outlook increased at our Minas-Rio iron ore operation in Brazil. In Copper, strong operational momentum and higher grades at both Quellaveco and Los Bronces underpinned performance, offsetting the current lower production phase at Collahuasi which is expected to recover by the end of 2026. In Iron Ore, Kumba had another solid quarter, with sales benefiting from improved rail performance, while at Minas-Rio we are increasing 2025 production guidance to 23-25Mt on the back of strong operational performance and following the successful completion of the 5-yearly pipeline inspection.

“In Steelmaking Coal, we continue to make progress towards a safe and structured restart and ramp up at Moranbah North ahead of resuming normal operations. At Grosvenor, we received approval from the regulator in August for first stage re-entry, marking a significant milestone in the recovery journey. Preparations are under way to restart the formal sale process of the Steelmaking Coal business in the coming months.

“We made further progress with our portfolio simplification, successfully divesting our residual c.19.9% interest in Valterra Platinum, raising cash proceeds of c.$2.5 billion. We continue to work through the regulatory approvals for the Nickel transaction and, for De Beers, we are making good progress with the dual track separation and a structured sale process is currently under way.

“Looking ahead, and building on the substantial value we have already unlocked through our own portfolio transformation, our agreement1 to merge with Teck represents our next major strategic step to accelerate value accretive growth, with the combined company forming a global critical minerals champion offering more than 70% copper exposure. Our recent agreement2 with Codelco to implement a joint mine plan for the adjacent Los Bronces and Andina operations in Chile serves as another example of delivering compelling industrial synergies as a means to drive our copper growth ambitions.”

Q3 2025 overview

| Production | Q3 2025 | Q3 2024 | % vs. Q3 2024 | YTD 2025 | YTD 2024 | % vs. YTD 2024 |

| Simplified portfolio | ||||||

| Copper (kt)(3) | 184 | 181 | 1% | 526 | 575 | (9)% |

| Iron ore (Mt)(4) | 14.3 | 15.7 | (9)% | 45.7 | 46.5 | (2)% |

| Manganese ore (kt)(5) | 973 | 406 | 140% | 2067 | 1,545 | 34% |

| Exiting businesses | ||||||

| Diamonds (Mct)(6) | 7.7 | 5.6 | 38% | 17.9 | 18.9 | (5)% |

| Steelmaking coal (Mt) | 1.9 | 4.1 | (54)% | 6.2 | 12.1 | (49)% |

| Nickel (kt) | 10.1 | 9.9 | 2% | 29.4 | 29.4 | 0% |

• Copper production was broadly flat at 183,500 tonnes, reflecting strong plant performance coupled with higher grades at both Quellaveco and Los Bronces, offset by lower production at Collahuasi due to lower grades and copper recovery. Quarter-on-quarter, production is 6% higher, as a result of strong plant performance at Quellaveco and Los Bronces.

• Iron ore production decreased by 9% to 14.3 million tonnes, primarily due to the expected lower production from Minas-Rio as a result of the planned pipeline inspection in August, which was successfully completed ahead of schedule.

• Manganese ore production increased by 140% to 972,800 tonnes, reflecting more normalised production levels following the temporary suspension caused by a tropical cyclone in March 2024. Export sales reached normalised levels in August.

• Rough diamond production increased by 38% to 7.7 million carats, primarily driven by higher production from Jwaneng in Botswana, in anticipation of the extended plant maintenance downtime in the fourth quarter.

• Steelmaking coal production was 54% lower at 1.9 million tonnes, primarily due to the incident at Moranbah North in March 2025 and the sale of Jellinbah in November 20247.

• Nickel production increased by 2% to 10,100 tonnes, reflecting the benefit of higher grades.

• Production and unit cost guidance for our continuing businesses remains unchanged for 2025, with the exception of Minas-Rio, where continued strong operational performance and the successful pipeline inspection have enabled an increase in guidance to 23-25 million tonnes (previously 22-24 million tonnes).