Anglo American (LON:AAL) has today announced its Production Report for the fourth quarter ended 31 December 2019.

Mark Cutifani, Chief Executive of Anglo American, said: “We have delivered our full year production targets across the business. Production is up 4%(1) for the quarter led by the continued successful ramp-up at Minas-Rio in Brazil. Increased production at Metallurgical Coal in Australia was offset by the drought in Chile impacting water availability at Los Bronces, as well as the anticipated lower production from De Beers as Venetia transitions to underground in South Africa and Victor reached the end of its mine life in Canada. As planned, we received the operating licence for the tailings dam raise at Minas-Rio before the end of 2019.”

Key highlights

• A 10%(2) increase in platinum and palladium volumes due to higher grades and throughput.

• Strong performance from Collahuasi as well as productivity improvements at Los Bronces have partially mitigated the impact of production losses at Los Bronces due to the continued drought.

• Continued strong performance from our Bulks business, reflecting the stability of operations under the Operating Model and progress in driving P101 levels of equipment performance to industry best practice and beyond.

• Minas-Rio continued its strong operational performance, with 6.2 million tonnes of high grade iron ore production in Q4. The tailings dam raise operating licence was received in December 2019.

• Kumba iron ore production of 11.8 million tonnes reflected improved run-rates following maintenance earlier in the year.

• Metallurgical coal production increased by 11% to 6.3 million tonnes due to the timing of longwall moves, as well as improved wash plant throughput and equipment efficiency.

| Q4 2019 | Q4 2018 | % vs. Q4 2018 | 2019 | 2018 | % vs. 2018 | |

| Diamonds (Mct)(3) | 7.8 | 9.1 | (15)% | 30.8 | 35.3 | (13)% |

| Copper (kt)(4) | 159 | 184 | (13)% | 638 | 668 | (5)% |

| Platinum (koz)(2)(5) | 532 | 485 | 10% | 2,051 | 2,021 | 1% |

| Palladium (koz)(2)(5) | 360 | 329 | 10% | 1,386 | 1,379 | 1% |

| Iron ore – Kumba (Mt) | 11.8 | 10.2 | 16% | 42.4 | 43.1 | (2)% |

| Iron ore – Minas-Rio (Mt)(6) | 6.2 | 0.2 | n/a | 23.1 | 3.4 | n/a |

| Metallurgical coal (Mt) | 6.3 | 5.6 | 11% | 22.9 | 21.8 | 5% |

| Thermal coal (Mt)(7) | 6.8 | 6.9 | (1)% | 26.4 | 28.6 | (8)% |

| Nickel (kt)(8) | 11.7 | 11.4 | 3% | 42.6 | 42.3 | 1% |

| Manganese ore (kt) | 903 | 972 | (7)% | 3,513 | 3,607 | (3)% |

(1) Copper equivalent production is normalised to reflect closure of Voorspoed and Victor (De Beers) and Sibanye-Stillwater Rustenburg material that has transitioned to a tolling arrangement (Platinum Group Metals). Excluding the impact of Minas-Rio, Group copper equivalent production is down 1% in the quarter.

(2) Normalised for the transition of Sibanye-Stillwater Rustenburg material from purchased concentrate to a tolling arrangement.

(3) De Beers production is on a 100% basis, except for the Gahcho Kué joint venture which is on an attributable 51% basis.

(4) Contained metal basis. Reflects copper production from the Copper business unit only (excludes copper production from the Platinum Group Metals business unit).

(5) Produced ounces of metal in concentrate. Reflects own mine production and purchases.

(6) Wet basis.

(7) Reflects export production from South Africa and attributable export production (33.3%) from Colombia.

(8) Reflects nickel production from the Nickel business unit only (excludes nickel production from the Platinum Group Metals business unit).

DE BEERS

Rough diamond production decreased by 15% to 7.8 million carats, driven by lower production levels in South Africa and Botswana. While trading conditions have improved since Q3 2019, production was reduced in response to softer rough diamond demand conditions experienced in the year.

Botswana production decreased by 7% to 5.9 million carats. Orapa production decreased by 29%, caused by a delay in an infrastructure project and expected lower grades. This was partially offset by a 21% increase at Jwaneng driven by planned increases in both tonnes treated and grade.

Namibian production decreased by 10% to 0.5 million carats, driven by Debmarine Namibia where production decreased by 9% to 0.4 million carats due to routine vessel maintenance in Q4 2019.

In South Africa, production decreased by 65% to 0.4 million carats due to lower volumes of ore mined at Venetia as it approaches the transition from open pit to underground. In addition, Voorspoed production ended in Q4 2018 when it was placed onto care and maintenance in preparation for closure.

Production in Canada decreased by 3% to 1.0 million carats, primarily due to the closure of Victor, which reached the end of its life in Q2 2019. Gahcho Kué production increased by 28% to 1.0 million carats due to strong plant performance.

Rough diamond sales totalled 7.0 million carats (6.6 million carats on a consolidated basis)(2) from two sales cycles, which compares with 9.9 million carats of sales (9.3 million carats on a consolidated basis)(2) from three sales cycles in Q4 2018.

For the full year, rough diamond sales volumes were 8% lower at 30.9 million carats (29.2 million carats on a consolidated basis)(2) compared with 33.7 million carats (31.7 million carats on a consolidated basis)(2) in 2018. In 2019, overall demand for rough diamonds was lower as a result of challenges in the midstream, with higher polished inventories and caution due to macro-economic uncertainty.

The full year consolidated average realised price of $137/ct was lower (2018: $171/ct), due primarily to a higher proportion of lower value rough diamonds sold in 2019 and a 6% lower rough diamond price index.

2020 Production Guidance

Production guidance for 2020(1) is unchanged at 32-34 million carats, subject to trading conditions. The higher production anticipates an improvement in trading conditions compared with 2019, and is driven by an expected increase in production from Venetia.

(1) De Beers Group production is on a 100% basis, except for the Gahcho Kué joint venture which is on an attributable 51% basis.

(2) Consolidated sales volumes exclude De Beers Group’s JV partners’ 50% proportionate share of sales to entities outside De Beers Group from Diamond Trading Company Botswana and the Namibia Diamond Trading Company, which are included in total sales volume (100% basis).

COPPER

Copper production decreased by 13% to 158,800 tonnes, largely impacted by a reduction at Los Bronces, driven by the continued drought conditions in central Chile, partially offset by continued strong plant performance at Collahuasi.

Production from Los Bronces decreased by 28%, to 71,700 tonnes with a 44% reduction in plant throughput (7 million tonnes vs 13 million tonnes) resulting from lower water availability. This was partly offset by strong mine performance, in particular a step-up in shovel productivity as a result of P101 improvements, and planned higher grades (0.99% vs. 0.81%). Chile´s central zone continues to face unprecedented climate conditions, with 2019 being one of the driest years on record and the driest since the start of the current decade-long drought.

At Collahuasi, attributable production increased by 4% to 72,200 tonnes, another record in copper concentrate production, with planned lower grades (1.25% vs 1.28%) more than offset by a strong plant performance that benefited from the ongoing long-term plant improvement plan.

2019 sales volumes were 643,900 tonnes, at an average realised price of 273c/lb ($6,019/t), in line with the average LME price.

2020 Production Guidance

Production guidance for 2020 is unchanged at 620,000-670,000 tonnes, subject to water availability.

PLATINUM GROUP METALS (PGMs)

Metal in concentrate production

Platinum and palladium production both increased by 10%, to 531,700 ounces and 360,400 ounces, respectively.

Own mined platinum production increased by 18% to 361,900 ounces and palladium production increased by 17% to 275,000 ounces. This was driven by increased production at Mogalakwena due to higher grade and throughput, and from Amandelbult, due to the ramp-up of the Dishaba lower section, as well as the inclusion of 100% of Mototolo volumes following the acquisition of the remaining 50% of the asset in November 2018. This was partially offset by the impact of Eskom power outages, which reduced overall own mined volumes by 8,500 platinum ounces and 6,000 palladium ounces.

Purchase of platinum in concentrate decreased by 5% to 169,800 ounces and purchase of palladium in concentrate decreased by 9% to 85,400 ounces, the result of lower purchases from joint ventures, as Mototolo became 100% owned in November 2018, as well as lower production from Bafokeng-Rasimone Platinum Mine.

Refined production and sales volumes

Refined platinum production(1) decreased by 18% to 629,700 ounces and refined palladium production(1) decreased by 20% to 396,600 ounces. Excluding the impact of the tolled volumes that were previously purchased as concentrate, refined platinum production was flat and palladium decreased by 6% as improved operational performance at the processing facilities was offset by the impact of Eskom power outages. These power outages in Q4 resulted in an inventory build-up of circa 45,000 platinum ounces and circa 27,000 palladium ounces.

Platinum sales volumes(1) decreased by 14% to 668,300 ounces and palladium sales volumes(1) decreased by 4% to 435,800 ounces due to lower refined production in the period.

The full year price per platinum ounce for the basket of metals sold increased by 27% to $2,819/ounce compared to 2018 due to 48% and 73% price increases in palladium and rhodium, respectively.

2020 Production Guidance

Production guidance (metal in concentrate) is unchanged at 2.0-2.2 million ounces of platinum and approximately 1.4 million ounces of palladium, subject to Eskom power performance.

(1) Does not include tolled volumes.

IRON ORE

Kumba – Total production volumes increased by 16% to 11.8 million tonnes, due to higher production at both Sishen and Kolomela.

Sishen’s production increased by 19% to 8.3 million tonnes as a result of improved operational performance in Q4 2019.

Kolomela’s production increased by 10% to 3.5 million tonnes, reflecting the ramp-up in production following the temporary closure of the DMS plant for an infrastructure upgrade in Q1 2019 and its subsequent re-opening, on schedule, in Q4 2019.

Total sales decreased by 10% to 10.5 million tonnes, driven by a 73% decline in domestic sales to 0.2 million tonnes due to lower domestic customer off-take with the winding down of the Saldanha Steel plant. Export sales were 5% lower at 10.2 million tonnes.

Total finished stock increased to 6.6 million tonnes(1) at Q4 2019 from 5.1 million tonnes at Q3 2019, as a result of lower domestic sales. Rail performance improved significantly in 2019, with port stock levels well set for Q1 2020.

In the fourth quarter, the average lump to fines ratio in the Kumba product was 66:34 (full year: 67:33), while the Fe content averaged 64.1% (full year: 64.2%).

The full year FOB realised price was $97/tonne, reflecting the reversal, driven by price movements, of gains from provisionally priced sales that supported the first half realised price of $108/tonne.

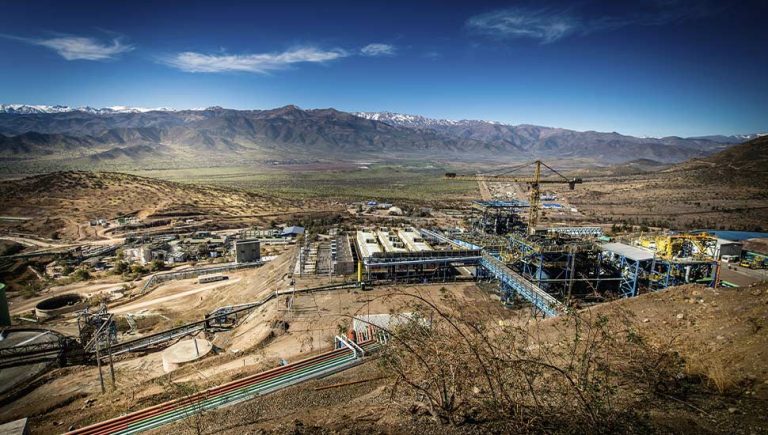

Minas-Rio – Production of 6.2 million tonnes was driven by continued strong operational performance, stability due to higher grade ore from the Step 3 mine area and productivity initiatives.

The construction of the tailings dam raise was completed in August 2019 and approval for the conversion of the installation licence to an operating licence was announced on 23 December.

The full year FOB realised price was $79/tonne, reflecting the reversal, driven by price movements, of gains from provisionally priced sales that supported the first half realised price of $92/tonne.

2020 Production Guidance

Kumba production guidance for 2020 is unchanged at 42-43 million tonnes.

Minas-Rio production guidance for 2020 is unchanged at 22-24 Mt, which includes a one-month production stoppage in Q2 to carry out routine internal scanning of the pipeline.

COAL

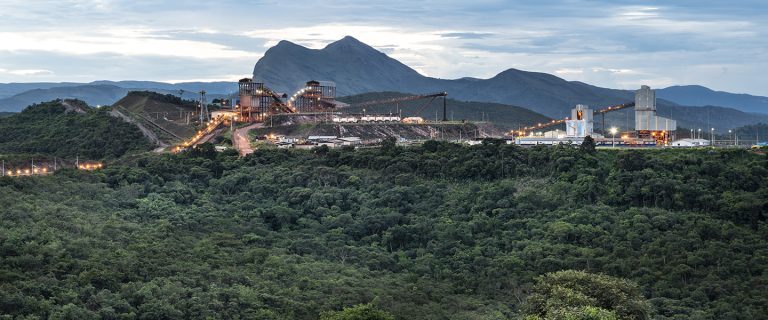

Metallurgical Coal – Export metallurgical coal production increased by 11% to 6.3 million tonnes primarily due to the timing of longwall moves at Grosvenor and Grasstree, as well as improvements in wash plant throughput at Moranbah-Grosvenor and equipment productivity at Dawson.

In the fourth quarter, the ratio of hard coking coal production to PCI/semi-soft coking coal was 81:19 (full year 2019: 83:17).

Thermal Coal South Africa – Export thermal coal production was flat at 4.5 million tonnes.

Thermal Coal Colombia – Attributable export thermal coal production decreased 2% to 2.3 million tonnes in response to weak market conditions.

The full year weighted average realised price for export thermal coal from South Africa and Colombia was $59/tonne. This was 10% lower than the weighted average quoted FOB price from South Africa and Colombia, due to lower than benchmark energy content coal from South Africa.

2020 Production Guidance

Metallurgical coal production guidance for 2020 is unchanged at 21-23 million tonnes. This reflects the sale of a 12% interest in the Grosvenor mine that is expected to complete during the year, equalising the ownership across the Moranbah-Grosvenor integrated operations.

Thermal coal production guidance for 2020 is unchanged at circa 26 million tonnes.

NICKEL

Nickel production increased by 3% reflecting improved operational stability.

2020 Production Guidance

Production guidance for 2020 is unchanged at 42,000-44,000 tonnes.

MANGANESE

Manganese ore production decreased by 7% to 902,900 tonnes, mainly due to mining fleet reliability issues in South Africa.

Manganese alloy production decreased by 17% to 31,600 tonnes due to a furnace outage in Australia.

| Manganese (tonnes) | Q4 | Q3 | Q2 | Q1 | Q4 | Q4 2019 vs. Q3 2019 | Q4 2019 vs. Q4 2018 | 2019 vs. 2018 | |||||

| 2019 | 2019 | 2019 | 2019 | 2018 | 2019 | 2018 | |||||||

| Samancor | |||||||||||||

| Manganese ore(1) | 902,900 | 910,400 | 826,100 | 874,000 | 971,900 | (1 | )% | (7 | )% | 3,513,400 | 3,606,500 | (3 | )% |

| Manganese alloys(1)(2) | 31,600 | 29,200 | 41,200 | 35,200 | 38,000 | 8 | % | (17 | )% | 137,200 | 156,800 | (13 | )% |

| Samancor sales volumes | |||||||||||||

| Manganese ore | 911,000 | 897,800 | 958,400 | 843,400 | 959,800 | 1 | % | (5 | )% | 3,610,600 | 3,534,500 | 2 | % |

| Manganese alloys | 27,200 | 30,400 | 44,800 | 30,100 | 44,000 | (11 | )% | (38 | )% | 132,500 | 161,100 | (18 | )% |

(1) Saleable production.

(2) Production includes medium carbon ferro-manganese.

EXPLORATION AND EVALUATION

Exploration and evaluation expenditure increased by 15% to $92 million. Exploration expenditure increased by 52% to $44 million driven by increased drilling activities in Copper, PGMs and Kumba Iron Ore. Evaluation expenditure decreased by 4% to $49 million largely due to decreased works in Copper, partially offset by increased spend in Metallurgical Coal, Thermal Coal and De Beers.

CORPORATE ACTIVITY AND OTHER ITEMS

During the quarter, charges recognised within EBITDA relating to rehabilitation provisions are currently estimated to be $0.1 billion at De Beers and $0.1 billion at Copper.

NOTES

• This Production Report for the quarter ended 31 December 2019 is unaudited.

• Production figures are sometimes more precise than the rounded numbers shown in this Production Report.

• Copper equivalent production shows changes in underlying production volume. It is calculated by expressing each product’s volume as revenue, subsequently converting the revenue into copper equivalent units by dividing by the copper price (per tonne). Long-term forecast prices are used, in order that period-on-period comparisons exclude any impact for movements in price.

• Please refer to page 16 for information on forward-looking statements.

In this document, references to “Anglo American”, the “Anglo American Group”, the “Group”, “we”, “us”, and “our” are to refer to either Anglo American plc and its subsidiaries and/or those who work for them generally, or where it is not necessary to refer to a particular entity, entities or persons. The use of those generic terms herein is for convenience only, and is in no way indicative of how the Anglo American Group or any entity within it is structured, managed or controlled. Anglo American subsidiaries, and their management, are responsible for their own day-to-day operations, including but not limited to securing and maintaining all relevant licences and permits, operational adaptation and implementation of Group policies, management, training and any applicable local grievance mechanisms.